Buying a home is one of the most exciting—and financially significant—decisions most people make. But with mortgage rates around 6%+ in late 2025, understanding how much house you can comfortably afford is more important than ever. Let’s break it down step by step and look at real-world numbers so you can house hunt with confidence.

🏡 1. Mortgage Rates Today — What Buyers Are Paying

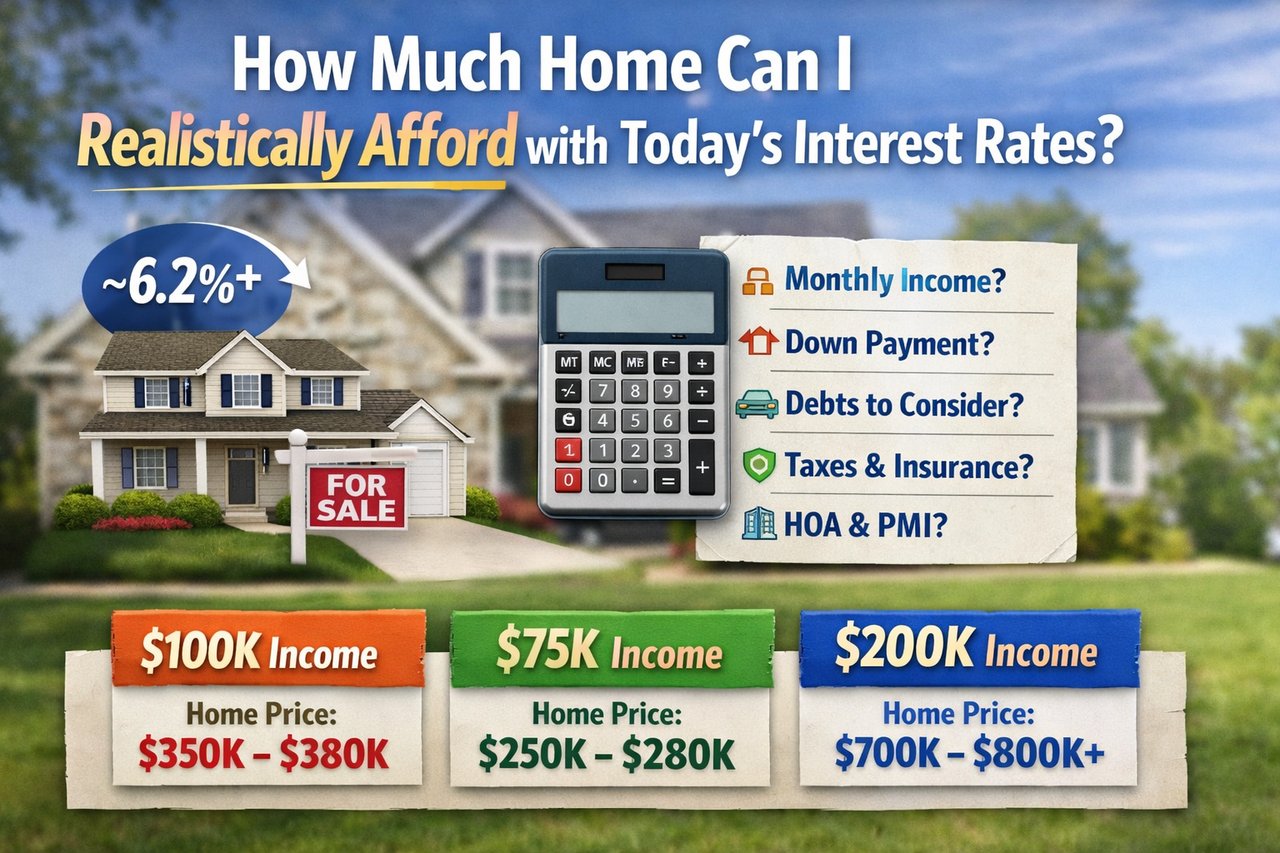

As of December 2025, the average 30-year fixed mortgage rate sits right around 6.2%-6.3%, depending on the lender, your credit, and your loan program. Bankrate

🔹 30-year fixed — ~6.26%

🔹 15-year fixed — ~5.64%

🔹 5/1 ARM — ~5.54%

These aren’t the ultra-low rates of 2020–2021, but they’re still close to long-term historical averages. The Mortgage Reports

📊 2. Affordability: It’s More Than Just the Rate

When people ask “how much home can I afford?”, lenders look at three core things:

-

Your Income

-

Your Debt Payments

-

Your Down Payment / Cash Available

And importantly — they include ongoing homeownership costs like:

-

Mortgage principal & interest

-

Property taxes

-

Homeowner’s insurance

-

Private mortgage insurance (if <20% down)

-

HOA dues (if applicable)

These affect your actual monthly payment. Zillow

🧮 3. Real-World Affordability Examples

Here’s how to think about actual numbers based on household income. The following are illustrative using general affordability guidelines (roughly keeping mortgage payment at ≤30–36% of gross monthly income):

💡 Example 1: $100,000 Household Income

-

Gross monthly income: ~$8,333

-

Safe monthly housing budget (30% rule): ~$2,500

-

With ~6.2% rate and typical taxes/insurance included, that budget might translate to a home price around $350,000 – $380,000 (estimate). Zillow

💡 Example 2: $75,000 Household Income

-

Gross monthly income: ~$6,250

-

30% housing budget: ~$1,875

-

Estimated affordable home price: $250,000 – $280,000

(This assumes modest taxes and insurance — local costs vary.) Zillow

💡 Example 3: $200,000 Household Income

-

Gross monthly income: ~$16,666

-

30% housing budget: ~$5,000

-

Estimated home price range: $700,000 – $800,000+

(This is a broad range because high incomes vary widely in local tax and insurance costs.) Zillow

🔎 Important: These numbers don’t include other debts (car loans, student loans, credit cards). Lenders use your debt-to-income (DTI) ratio to ensure total monthly debt stays manageable. Zillow

These examples are general estimates — to get a more accurate figure, use an affordability calculator like those from Zillow, Rocket Mortgage, Bankrate, or Freddie Mac. Zillow+1

🧾 4. What Else Should You Factor In?

📌 Property Taxes

Property tax rates vary widely by location. Two homes with the same price can have very different monthly tax costs — so factor this early.

📌 Homeowner’s Insurance

This isn’t optional — it’s required for nearly all mortgages and varies by state and risk factors. NerdWallet

📌 HOA Fees

Communities with amenities like pools or lawn care come with monthly HOA dues — sometimes hundreds of dollars more. NerdWallet

📌 Down Payment & PMI

Putting 20% down lowers your monthly payment and avoids Private Mortgage Insurance (PMI), which can add hundreds per month if you put <20% down. NerdWallet

📉 5. What Mortgage Rates Mean for Your Budget

Even small changes in interest rates make a big difference in monthly payment — and affordability.

For example:

-

On a $400,000 mortgage, moving from 6% to 7% could increase your monthly payment by hundreds of dollars, even before taxes/insurance. Kiplinger

This is why it’s critical not just to qualify for a loan, but to feel comfortable with the payment.

🛠 6. Tools to Help You Calculate Your Number

Here are some tools you can use to personalize your affordability:

🔗 Zillow Affordability Calculator — Helps estimate a comfortable monthly payment and max home price based on your income, debt, and down payment. Zillow

🔗 Freddie Mac Affordability Calculator — Personalized guidance based on your budget and loan info. My Home

🔗 Rocket Mortgage Calculator — Lets you adjust income, debt, credit score, and local tax/insurance. Rocket Mortgage

🔗 Bankrate Mortgage Calculator — Great for side-by-side comparisons of different scenarios. Bankrate

Plug in your real numbers — it’s the best way to see exactly what you can afford.

📌 Final Takeaway

Affordability isn’t just about what a lender will approve — it’s about what fits your life and goals. At today’s rates (roughly 6.2%–6.3% on a 30-year fixed mortgage), being thoughtful about income, debts, taxes, insurance, and future plans will help you choose a home that feels right — not just possible. Bankrate

If you’d like help crunching your exact numbers or want a personalized affordability plan for Hickory or the Catawba Valley, we’d be happy to walk you through it!